A customer once told us he spent 45 minutes at a rental desk trying to understand the difference between CDW, Super CDW, Theft Protection, and Full Coverage Waiver. The agent kept using terms like "deductible," "excess," and "irreducible deposit" without explaining what any of them actually meant. He walked away paying double his advertised rate and still wasn't entirely sure what he'd bought.

This is not an unusual story. Insurance is where car rental companies in Morocco make their real money. That advertised 30-euro daily rate becomes 60 euros after the desk agent finishes their upsell pitch. The good news is that the desk is not your only option. Third-party rental insurance bought before you travel can cover the same risks at a fraction of the cost.

What You'll Learn in This Guide

- What insurance is legally required for car rentals in Morocco and what's automatically included

- The difference between CDW, excess waiver, and third-party liability in plain language

- Why desk-purchased waivers cost more than equivalent third-party coverage

- The critical warning about credit card insurance and Morocco

- How LiloxCars insurance works and why it removes the upsell conversation entirely

What Moroccan Law Requires and What's Automatically Included

Morocco requires all vehicles on the road to be insured, including rental cars. A Collision Damage Waiver is required to rent a car in Morocco and is usually included in your rental. This means the base rental rate at every legitimate company in Agadir already includes at minimum a CDW and third-party liability coverage. You cannot drive away from a rental desk in Morocco without any insurance. The question is not whether you have coverage but how much excess you're carrying and what the policy excludes.

CDW waives damage costs but with a high excess payable for damages. Some types of damage are not covered by CDW, for instance some rental companies do not cover windscreens, cracks and chips, tyre punctures and replacements, and damages to headlights and underbody. This is where the desk upsell begins. The included CDW has gaps, and the agent's job is to sell you products that fill them.

The Insurance Products You'll Be Offered at the Desk

Understanding what each product actually does removes the confusion that makes desk upsells so effective.

Collision Damage Waiver (CDW) reduces your liability for damage to the rental vehicle. It does not eliminate it entirely unless you purchase a zero-excess upgrade. The standard CDW included in your base rental carries an excess of typically €1,000 to €3,000 depending on the company and vehicle category.

Super CDW or Excess Waiver reduces your remaining excess toward zero. This can be purchased for $30 to $45 per day at the desk, with price tiers meaning you pay even more to get a zero excess. On a seven-day rental this adds €200 to €300 or more to your total cost.

Theft Protection covers you in the event the vehicle is stolen. It is sometimes bundled with CDW as LDW, and sometimes sold separately.

Personal Accident Insurance covers medical costs for the driver and passengers in the event of an accident. This is optional at the rental desk for $10 to $15 per day and is also available in standard travel insurance policies. If your travel insurance already covers medical costs abroad, this is a direct duplication.

Roadside Assistance covers towing, fuel delivery, and key lockout. This costs $10 to $15 per day at the desk. Some third-party providers include it as standard at no extra charge.

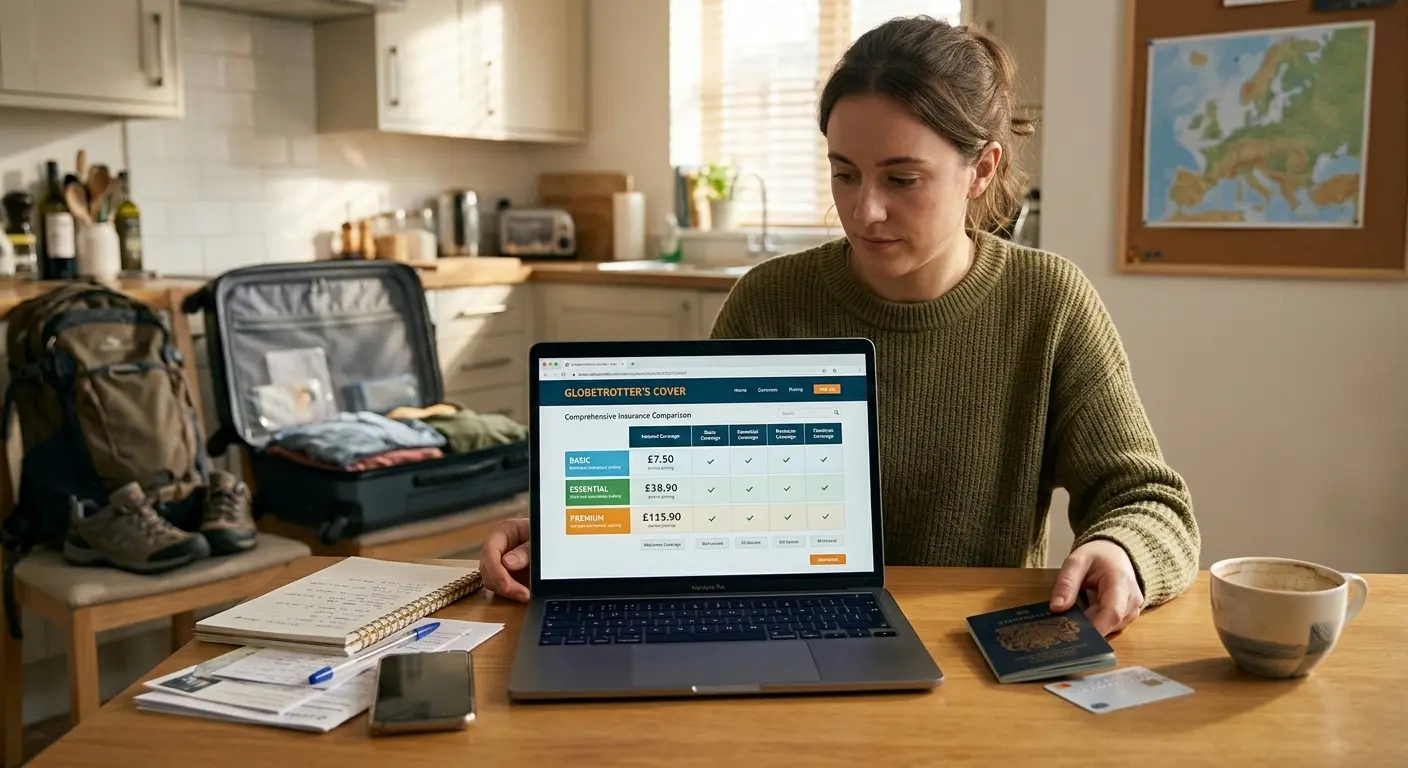

Why Third-Party Insurance Is Usually Cheaper

Third-party providers have built a global business around saving customers 50 percent versus equivalent coverage at the rental desk. The mechanics are straightforward. Third-party insurers buy coverage in volume, operate at lower margins than rental desks, and sell direct to travelers before they reach the pressured environment of the pickup counter.

Booking your excess car rental insurance beforehand is half the price compared to booking it later at the counter. Providers like RentalCover, InsureMyRentalCar, and Allianz offer excess waiver policies specifically for rental cars that can be purchased online before you travel. You pay the rental company's base rate at pickup, decline the desk upsell, and rely on your pre-purchased third-party policy for excess coverage.

The process when something goes wrong: the rental company charges your card for the damage up to the excess amount. You then submit a claim to your third-party insurer with the documentation and receive reimbursement. Some providers aim to pay 98 percent of claims within 3 business days.

The Critical Warning About Credit Card Insurance in Morocco

Many travelers assume their premium credit card's rental car coverage handles this automatically. In Morocco, this assumption carries real risk.

Many premium credit cards explicitly list Morocco in their country exclusion lists due to high-risk classification. The risk of finding out your card doesn't cover you after an incident has occurred is far too great. This mistake can cost you thousands, turning your dream vacation into a financial nightmare.

Before you travel, call your credit card provider and ask specifically whether rental car coverage applies in Morocco and whether it covers the full excess amount. Get the answer in writing if possible. Do not assume it applies because it worked in France or Spain. Morocco is frequently excluded where other destinations are not.

What to Look for in a Third-Party Policy for Agadir

Not all third-party policies are equal. Before you purchase, confirm the following:

- The policy explicitly covers Morocco, not just "worldwide" in general terms

- The excess reimbursement limit is equal to or greater than the excess on your rental contract

- Windscreen, tyre, and undercarriage damage are included, as these are the most common exclusions

- The claims process is clear and the timeline for reimbursement is stated

- Roadside assistance is included or available as an add-on

Do not wait until you are tired and jet-lagged at the rental counter to figure this out. Choose your approach before you travel and buy your policy from a reputable provider, reading reviews and ensuring it explicitly covers Morocco.

How LiloxCars Insurance Works and Why It's Different

We include full insurance with a €1,000 excess in every rental as standard. There are no tiers to navigate, no upsell conversation at pickup, and no pressure to add products you don't understand. The excess amount is stated clearly in your booking confirmation before you arrive.

Because our excess is fixed at €1,000 and stated upfront, if you want to cover that amount with a third-party excess waiver policy, you know exactly what limit to buy before you travel. There are no surprises at the desk that change the calculation.

We don't charge a deposit against that excess either. No amount is frozen on your card at pickup. If something happens during your rental, we handle it directly and fairly without pre-emptive card holds complicating the conversation.

Questions We Get Asked All the Time

Is it safe to decline the insurance upsell at the Agadir rental desk if I have third-party coverage?

Yes, provided your third-party policy explicitly covers Morocco, covers the full excess amount on your contract, and includes the exclusions that matter most for Moroccan roads such as windscreen and tyre damage. Have your policy document accessible at pickup so you can refer to it confidently.

Does LiloxCars require me to purchase additional insurance?

No. Full insurance with a €1,000 excess is included in your rental. We don't offer or pressure additional insurance products at pickup. What's in your booking confirmation is what you have.

What happens if I damage the car during a LiloxCars rental?

Your liability is capped at the €1,000 excess stated in your contract. We handle the process directly with you via WhatsApp. If you have a third-party excess waiver policy, you can submit the documentation to your insurer after settling with us and recover the cost through their claims process.

Is personal accident insurance worth buying separately for Morocco?

If your travel insurance already includes medical coverage abroad, personal accident insurance from the rental desk is a duplication. Check your travel policy specifically for Morocco coverage and medical evacuation before you decide. If it's comprehensive and Morocco is included, the desk add-on is unnecessary.

Can I buy third-party rental insurance after I've already booked the car?

Yes. Most providers let you purchase a policy up until the day of rental. Buying earlier is better because it gives you time to read the terms and confirm Morocco is covered. Last-minute purchases under time pressure replicate exactly the same conditions that make desk upsells effective.

The Desk Upsell Is Optional. The Research Before You Travel Is Not.

Third-party rental insurance for Agadir is a legitimate, cost-effective alternative to paying desk waiver rates. It requires a small amount of research before you travel, a clear understanding of what your policy covers, and the confidence to decline the counter upsell when you know your coverage is already in place.

If you want to skip the insurance conversation entirely, you can book with LiloxCars directly and arrive knowing full coverage is already included in your rate, with the excess clearly stated and no deposit held on your card.